It probably happened in a quiet moment. Maybe you were rocking a newborn at 2 a.m. Maybe you were signing mortgage papers and felt the weight of that number land in your chest. Whatever the moment, the question surfaced: That one question that sits at the heart of Canadian family protection: What if something happened to me?

If you didn’t have a clear answer, you’re not alone. According to a 2024 study by PolicyMe, 42% of Canadians don’t have life insurance, or aren’t sure whether they do. This blog exists to change that.

Every type of insurance you’ll ever need maps back to one of two questions. Once you understand this, the entire world of insurance becomes dramatically less confusing.

Watch: The 6 layers explained in plain language

The two questions that actually matter in shaping a Canadian Family Protection plan

Every type of insurance you’ll ever need i.e. life, disability, health, home, critical illness, maps back to one of two questions. Once you understand this, insurance becomes dramatically less confusing.

What’s at stake if life is short

- Your income disappears overnight. Everything your household pays for; the mortgage, groceries, childcare etc is tied to you being alive and earning.

- Debt doesn’t die with you. Your mortgage and loans become your family’s problem the moment you’re gone.

- Childcare costs. A surviving spouse may suddenly need full-time childcare on a single income.

What’s at stake if life is long

- You’re more likely to be disabled than to die early. The Canadian Life and Health Insurance Association (CLHIA) estimates that 1 in 3 Canadians will experience a disability lasting longer than 90 days during their working life.

- Provincial health care has gaps. Dental, prescriptions, vision, physio, and mental health services are largely out-of-pocket.

- Group disability coverage is often inadequate. It replaces only 60–70% of income, uses broad definitions, and vanishes when you change jobs.

The 6 layers of the Canadian family protection plan

Think of the Canadian family protection plan as having six layers, each addressing a specific financial risk. Together, they form a complete safety net.

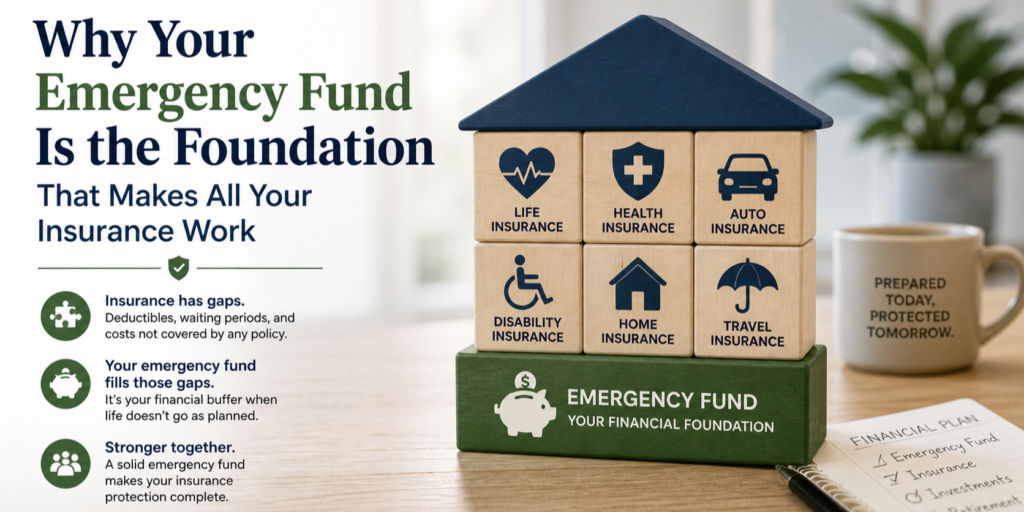

Target: 3–6 months of essential living expenses

| What it covers | Why insurance alone isn’t enough |

|---|---|

| Insurance deductibles | You pay before coverage kicks in. |

| Disability waiting period | Benefits can take 90–120 days to start. |

| Job loss bridge | EI covers only ~55% of lost active income. |

| Home/car repairs | Small claims aren’t worth making. |

| Medical out-of-pocket costs | Provincial gaps add up quickly. |

Answers: What if life is short?

Answers: What if life is long?

Answers: What if life is long?

Answers: What if life is short?

Answers: Is my coverage keeping up with my life?

| Life Event | What to Review |

|---|---|

| Getting married | Beneficiary designations, combining policies |

| Having a baby | Life insurance amount, health plan additions |

| Buying a home | Home insurance, mortgage protection |

| Changing jobs | Group benefits portability, coverage gaps |

| Turning 40 | Full insurance audit, critical illness review |

Pro tip: Life insurance premiums increase by roughly 8% for every year you wait. The best time to buy was five years ago. The second best time is today.