All insurance in Canada falls into one of two regulated branches. Once you understand these two types of insurance, what’s in each branch, who sells it, and who regulates it, the entire insurance landscape becomes more navigable.

If you’ve ever felt overwhelmed by insurance, it’s likely because you encountered individual products – term life, disability, tenant insurance, critical illness – without understanding the framework that connects them. You were handed leaves without ever seeing the tree.

This post shows you the tree.

Every insurance product available to Canadians belongs to one of two branches. These aren’t informal categories, they are the actual regulatory divisions that govern how insurance companies are licensed, how advisors are certified, and how consumers are protected in Canada. Understanding them takes about ten minutes. Using them takes the rest of your life.

The two types of insurance in Canada

Type 1: Life & health insurance

Protects people; your life, your income, and your health.

The question it answers: What happens to my family or to me if something happens to my body, my health, or my ability to earn?

- Term life insurance

- Permanent life insurance

- Disability insurance

- Critical illness insurance

- Health & dental insurance

- Long-term care insurance

Type 2: Property & casualty insurance

Protects things; your home, your vehicle, and your liability to others.

The question it answers: What happens to my assets — or my finances — if something is damaged, stolen, destroyed, or I’m held legally responsible?

- Home insurance

- Condo insurance

- Renters / tenant insurance

- Auto insurance

- Business insurance

- Personal liability insurance

Regulated by IBC & provincial bodies

Why “life and health” and not just “life”? The “and health” does real work. Disability insurance, critical illness coverage, and extended health plans are all sold by life insurance agents under a life licence not by property and casualty brokers. In Canada, if a product protects something that happens to a person’s body, health, or ability to earn, it belongs to the life and health branch. That’s the regulatory logic, and it maps onto the products you’ll actually encounter.

Why this matters practically: A life insurance broker and a home insurance broker are specialists in different branches. When you’re shopping for life insurance, you want a licensed life insurance advisor. When you’re shopping for home insurance, you want a property and casualty (P&C) broker. Working with the right specialist ensures you’re getting expert guidance not a generalist covering two very different fields.

Ultimately, being knowledgeable about the types of insurance helps you protect what matters.

The one question that sorts all of insurance

There is a single question you can ask about any insurance product, any product, that will help you determine which of the two types of insurance you should be considering.

This isn’t a simplification. It’s exactly how Canadian insurance regulation works. OSFI supervises life insurance companies and P&C companies through entirely separate divisions because the risk profiles, capital requirements, and product structures of the two branches are that different. Two separate regulatory worlds, divided by one question.

Life & health insurance: the complete map

The life and health branch covers every financial risk tied to a human being. In Canada, selling these products requires a life insurance licence issued under the Life Licence Qualification Program (LLQP) and governed provincially. The Canadian Life and Health Insurance Association (CLHIA) represents this industry nationally.

Life & health insurance

Protects people and income

Term life

Pays a tax-free lump sum to your beneficiaries if you die within a fixed term. The term is the period during which the coverage is guaranteed to stay in place as long as premiums are paid. Common terms are 10 and 20 years, though 15, 25, and 30-year terms are also available from some insurers. The most affordable and widely applicable life product, the preferred starting point for most young Canadian families.

What if I die before my mortgage is paid and before my children are grown?

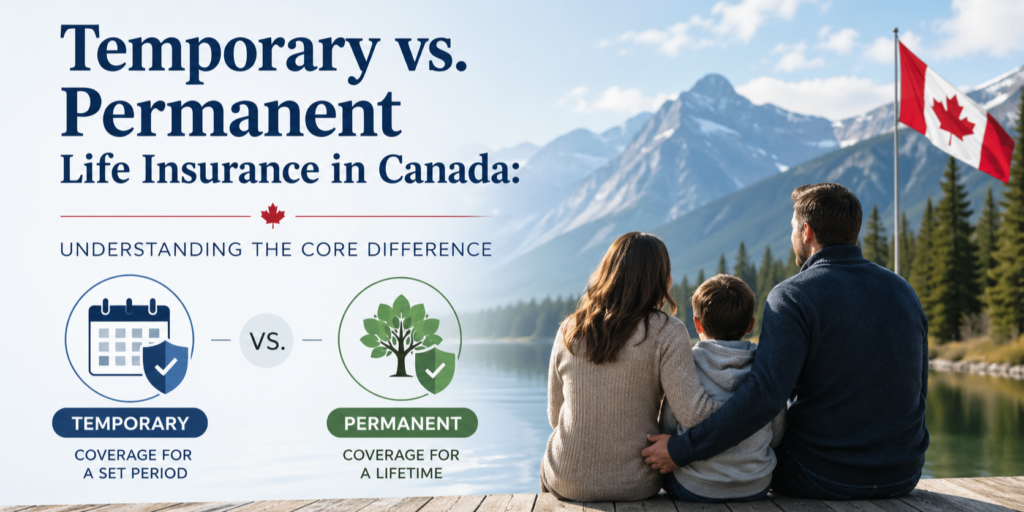

Permanent life

Lifetime coverage that never expires as long as premiums are paid. Builds cash value on a tax-advantaged basis. Includes whole life (insurer manages investments), and universal life (self-directed investment component). Used for estate planning, wealth transfer, and business succession.

What if I need lifetime coverage or estate planning?

Disability

Replaces a portion of your income if you cannot work due to illness or injury. This is accident and sickness (A&S) insurance sold under a life licence. According to the CLHIA’s Guide to Disability Insurance, 1 in 3 Canadians will be disabled for 90 days or more before age 65. The most underused protection in Canada.

What if I can’t work for a year or longer?

Critical illness

Pays a tax-free lump sum upon diagnosis of a covered condition. Typically conditions covered are cancer, heart attack, or stroke. Also A&S insurance, sold under a life licence. You use the money however you need: treatment costs, time off work, debt repayment, vacation. Your choice. Complements disability insurance; does not replace it.

What if I’m diagnosed with cancer?

Health & dental

Extended health and dental plans that cover what provincial health care doesn’t. Things like prescription drugs, dental care, vision, physiotherapy, mental health, and paramedical services. Also A&S insurance under a life licence. See Canada.ca for what your province covers and what it doesn’t.

What do my provincial benefits not cover?

Long-term care

Covers the cost of personal care services if aging, chronic illness, or disability limits your ability to care for yourself independently. Most relevant later in life but qualifying health standards only rise with age, so planning early matters. With nursing home costs running as high as $5,000/month in Canada, this is a gap worth taking seriously.

What if I need care in my 70s or 80s?

Travel insurance

Covers medical emergencies, hospitalization, and emergency evacuation when you travel outside your province or country. The medical component is Accident and Sickness insurance sold under a life licence. This is why travel medical insurance comes from the same licensed advisors who sell disability and critical illness coverage. Your provincial health plan provides very limited coverage outside Canada, and none at all in many situations. For Canadians who travel regularly, travel medical insurance is one of the most commonly needed and most commonly overlooked coverages in the life and health branch.

What if I have a medical emergency abroad?

Mortgage and credit insurance

Pays off a specific debt – typically a mortgage, credit card balance, or loan – if you die or become disabled. In Canada, banks and lenders sell this as creditor insurance at the point of borrowing. It is technically a life and health insurance product sold under a life licence, which means it belongs to this branch despite being offered by a financial institution rather than a life insurance advisor.

There is an important distinction worth understanding before you sign up for it at the bank. With creditor insurance, the lender is the beneficiary, and not your family. The benefit decreases as your balance decreases, while your premium stays the same. A personally owned term life insurance policy, by contrast, pays your family directly and gives them the flexibility to decide how to use the money. The Financial Consumer Agency of Canada has published a plain-language comparison of mortgage creditor insurance versus personally owned life insurance — worth reading before you sign anything at the bank.

What if I die before my mortgage is paid off?

A&S sits inside the life branch and that matters. Disability, critical illness, and extended health are all classified as Accident and Sickness (A&S) insurance in Canada. They are sold by life insurance agents, not P&C brokers. This is why your disability insurance and your home insurance come from different advisors. They are licensed under completely different regulatory streams that represent the 2 types of insurance pointed out in this article. When you need a disability or health product, go to a life-licensed advisor. Not a P&C broker.

A note on trip cancellation and baggage coverage. Travel insurance is sold as a bundled product that typically combines travel medical (life and health branch) with trip cancellation, trip interruption, and baggage loss coverage (property and casualty branch). When you buy a travel insurance package, you are often buying across both regulatory branches at once. This is one of the few places where the two types of insurance overlap inside a single product. Always confirm what is covered under each component before you travel.

Property & casualty insurance: the complete map

The P&C branch covers every financial risk tied to a physical asset or legal liability. Selling these products requires a P&C broker or agent licence which is also provincially governed. The Insurance Bureau of Canada (IBC) represents this industry nationally. OSFI supervises federally incorporated P&C insurers for financial soundness; provincial bodies handle market conduct.

Property & casualty insurance

Protects assets and liability

Home insurance

Covers the structure of your home and its contents against fire, theft, water damage, and other covered perils. Also includes personal liability coverage. Required by virtually all Canadian mortgage lenders. Canada recorded over $8 billion in insured catastrophe losses in 2024; a record driven by floods, wildfires, and severe storms.

What if my house burns down, floods, or is broken into?

Tenant insurance

Protects renters’ personal belongings, personal liability, and additional living expenses if the unit becomes uninhabitable. Starting from roughly $15–$25/month, it is one of the most affordable and overlooked products in Canada and yet a significant number of Canadian renters carry none. Your landlord’s policy does not cover your belongings.

What if my apartment is broken into or damaged?

Condo insurance

Covers your unit’s interior, personal belongings, and personal liability. Your condo corporation’s master policy covers the building exterior and common areas only. Your unit and everything inside it is your responsibility. IBC’s condo insurance guide explains the split clearly.

What does my condo corp NOT cover?

Auto insurance

Mandatory in every Canadian province and territory. Covers third-party liability (injury and property damage to others), accident benefits, and optionally collision and comprehensive coverage for your own vehicle. How rates are set and claims are handled varies significantly by province. Some operate public systems (BC, Manitoba, Saskatchewan, Quebec), others private.

One important Canadian distinction: four provinces operate public auto insurance systems rather than private ones. British Columbia is served by ICBC, Manitoba by Manitoba Public Insurance, Saskatchewan by SGI, and Quebec by the SAAQ for bodily injury liability (though property damage coverage in Quebec remains privately purchased). In these provinces, you purchase your mandatory coverage directly from the public insurer rather than through a private P&C broker. The coverage structure and claims process differ from province to province. If you live in or are moving to one of these provinces, the relevant public insurer’s website is your primary resource for understanding how auto coverage works in your specific situation.

What if I cause an accident?

Liability insurance

Protects you if you’re legally responsible for bodily injury or property damage to someone else. Included within home and tenant policies as standard. Umbrella or excess liability policies extend this protection well beyond standard limits for households with greater exposure.

What if someone sues me?

Pet insurance

Covers veterinary costs if your pet is injured or becomes ill. In Canada, pet insurance sits within the property and casualty branch because it protects an asset rather than a person. It is not a regulated mandatory coverage, but it is one of the fastest-growing insurance categories among young Canadian families. Veterinary costs in Canada can run into thousands of dollars quickly — a single emergency surgery can exceed $5,000. Premiums vary widely based on your pet’s breed, age, and the coverage level you choose, but basic accident and illness plans typically start around $30 to $60 per month for a dog. Pet insurance is purchased through P&C brokers, directly through insurers, or increasingly through digital platforms.

What if my pet needs emergency surgery or ongoing treatment?

Finding the gaps in your coverage

Most Canadians have some coverage in both types of insurance but almost everyone has gaps. Use these questions to identify where yours might be:

Your coverage gap finder

Answer honestly. These reveal where you’re exposed

If you died tomorrow…

Could your family pay the mortgage, raise the kids, and replace your income? If not – you have a life insurance gap.

If you couldn’t work for 2 years…

Could your household survive on your savings and your partner’s income alone? If not – you have a disability insurance gap.

If you had a dental emergency…

Would a $2,000 root canal and crown cause financial stress? If yes — you have a health insurance gap.

If your home burned down…

Could you cover your living expenses for 3 months while it was rebuilt? If not — check your additional living expenses limit.

If you rent and have no tenant insurance…

Could you replace everything you own after a theft or fire? If not — you have a property gap for under $20/month.

If you were diagnosed with cancer…

Could you take 6 months off work and fund treatment costs not covered by provincial health? If not — consider critical illness insurance.

Two types of insurance, two licensed specialists

This is the practical implication of the two-branch structure that most Canadians have not averted their minds to: the person who sells you life insurance and the person who sells you home insurance are licensed under completely different regulatory systems. They cannot do each other’s job. Working with the right specialist for the right branch is where getting good advice starts.

One footnote worth knowing: some advisors hold both a life insurance licence and a P&C licence, allowing them to sell products from both types of insurance. When this is the case, ask what licences they hold before the conversation goes further. Knowing the answer helps you understand what they can offer, what falls outside their scope, and whether you’ll need a second specialist for the other branch.

Where to start: the right coverage order

Both types of insurance matter but not all products matter equally at every stage of life. For most young Canadian families, this is the order in which protection should be built.

- Emergency fund – 3 to 6 months of essential expenses in a TFSA or HISA (high interest savings account). Not insurance at all, but the foundation that makes everything else work. Covers deductibles, elimination periods, and every gap insurance leaves behind.

- Disability insurance (life and health branch): protects your income, which is your most valuable financial asset. Statistically more likely to be needed before 65 than life insurance, and the most overlooked coverage in Canada.

- Life insurance (life and health branch): essential the moment you have dependents or significant debts. Premiums increase with every year you wait, and your insurability can change with your health at any time.

- Home or tenant insurance (P&C branch): required by mortgage lenders; critical for renters at ~$20/month. Protects the physical assets you’re building and covers your personal liability.

- Health & dental insurance (life and health branch): fills provincial gaps. Especially important without employer group benefits, or when self-employed.

- Critical illness insurance (life and health branch): a meaningful layer on top of the others. Pays a tax-free lump sum on diagnosis of cancer, heart attack, or stroke. This is often when you need financial flexibility most.

Know the map. Fill the gaps.

Take our free quiz to determine where the gaps are with your family protection plan.