Term life insurance is where most Canadian coverage plans begin and for good reason. It is the most affordable way to protect the people who depend on your income, the mortgage they depend on you to pay, and the future you are building together. This guide explains how it works, what it actually costs, and where it fits in your family’s protection plan. No jargon. No sales pitch.

Let’s start with the honest version of the conversation nobody had with you before you had kids, signed a mortgage, or built a life that other people depend on.

If you died tomorrow, your family would face a financial crisis and not just an emotional one. The mortgage payment would still arrive on the first of the month. Childcare would not stop costing money. Groceries, utilities, debt repayments, none of it pauses for grief.

Term life insurance in Canada is the financial tool designed to handle exactly that scenario. And for most young Canadians, it is the single most important coverage decision you will ever make.

42%

of Canadians have no life insurance or don’t know if they do – PolicyMe 2025

8%

Premium increase for every year you delay buying coverage – Ratehub

~$25/mo

Average cost of $500K term life insurance coverage for a healthy 30-year-old

What Is Term Life Insurance, really?

Term life insurance is a policy that pays a tax-free, lump-sum benefit to your named beneficiaries e.g. your partner, your children, or your estate if you die while the policy is active.

You choose three things when you apply:

The coverage amount – the death benefit your family receives (e.g., $500,000, $1,000,000). This is paid out completely tax-free.

The term length – how long the policy covers you (typically 10, 20, or 30 years). Premiums are fixed for this entire period.

Your beneficiaries – who receives the money. You can name multiple people and specify what percentage each receives.

Term life policies can also be structured as joint policies covering two lives under a single contract. This is typically offered as first-to-die (the benefit pays when the first partner dies) or last-to-die (the benefit pays when the surviving partner dies). Joint policies are worth considering for couples who want simplified coverage under one contract, though it is generally recommended to compare the total cost of two individual policies before choosing a joint structure, as individual policies offer more flexibility when life circumstances change.

In return, you pay a fixed monthly or annual premium for the duration of that term. If you die within the chosen term, your beneficiaries receive the full coverage amount. If you outlive the term of your term life policy, which, statistically, most people do, the policy simply expires with no payout and no cash value.

That last part is where people sometimes balk. “What! You mean I could pay premiums for 20 years and get nothing?” Yes! But you didn’t get nothing. Your family was protected for 20 years. If you had passed during that time, your family would have maintained the life you were giving them before you died. The fact that you didn’t die is the good news, not the bad news.

How Term Life Insurance Works in Canada: Step by Step

The mechanics are refreshingly simple compared to most financial products.

⏱ The free look period – use it deliberately

Most Canadian insurers offer term life insurance policies with a review period of 10 to 30 days after your policy is issued. During this window, you can cancel for any reason and receive a full refund of all premiums paid. Do not let this window pass without doing four things:

- Read the exclusions section carefully and confirm nothing surprises you

- Verify that the conversion privilege is included and note the conversion deadline age

- Confirm your beneficiary designations are recorded exactly as intended

- Check that the coverage amount and term length on the policy document match what you applied for. Errors on issued policies are rare but they do happen

What Term Life Insurance Does Not Cover

Term life insurance pays the death benefit in the vast majority of claims. But there are specific circumstances where a claim can be denied. Understanding these upfront is not pessimism, it is the foundation of your beneficiaries’ financial security.

Common exclusions to know

Most Canadian term life policies exclude the following circumstances. These exclusions vary by insurer and are listed in full in your policy document.

Suicide

Death by suicide within the first two years of the policy. Most insurers will return the premiums paid but will not pay the full death benefit. After two years, suicide is generally covered under standard Canadian term policies.

Misrepresentation

Death resulting from an undisclosed pre-existing condition. If you failed to disclose a condition during underwriting and that condition contributes to your death, the insurer may deny the claim on grounds of material misrepresentation. Always disclose everything, even conditions that feel minor or well-managed.

Excluded activities

Some policies exclude deaths resulting from specific high-risk activities such as base jumping, free solo climbing, or similar extreme sports. These exclusions vary by insurer. If you participate in high-risk activities, disclose them during underwriting and ask specifically about policy exclusions before signing.

Illegal activity

Most policies will not pay the death benefit if you die while committing a criminal act. The specific language varies by policy.

Substance abuse

Deaths directly caused by drug or alcohol abuse are typically excluded, particularly if the condition was not disclosed during the application process.

The two-year contestability period. Every term life insurance policy issued in Canada includes a contestability period, typically the first two years the policy is active. During this window, if you die, your insurer has the right to investigate the claim in full. If they find that material information was misrepresented or omitted on your application, a health condition you did not disclose, a medication you failed to mention, smoking status you understated, they can deny the claim and return only the premiums paid. After the two-year contestability period closes, the policy becomes incontestable on the grounds of misrepresentation. This is why complete honesty during the application process is not just ethical. It is what your family’s financial security is built on. Do not treat it lightly.

The practical rule: Disclose everything honestly during underwriting, read the exclusions section during your free look period, and keep a copy of your original application alongside your policy documents so your executor has full context if a claim is ever required.

What Does Term Life Insurance Cost in Canada?

This is the question that keeps people from acting and the answer almost always surprises them. PolicyMe reports the average cost of term life insurance starts at around $20–$30 a month for a healthy Canadian in their 30s. For a coverage amount that could pay off your mortgage, fund your children’s education, and replace years of income, that is less than most Canadians spend on a streaming subscription. Let that sink in.

According to the Canadian Life and Health Insurance Association, 23 million Canadians carried life insurance in 2024, with average household coverage sitting at $509,000 which is up 5.4% from the year prior. Term life policies now account for 66% of all individual life insurance in force in Canada, up from just 59% a decade ago, reflecting a clear shift toward the more affordable and flexible option. The pattern is consistent: as Canadians face larger mortgages, rising childcare costs, and longer financial commitments, the appetite for straightforward term coverage grows with it.

Estimated monthly premiums: $500,000, 20-year term

Age

Female (non-smoker)

Male (non-smoker)

| 25 | ~$18–$22 | ~$22–$28 |

| 30 | ~$20–$26 | ~$26–$34 |

| 35 | ~$26–$34 | ~$34–$44 |

| 40 | ~$38–$50 | ~$50–$68 |

| 45 | ~$60–$80 | ~$80–$105 |

| 50 | ~$95–$130 | ~$130–$175 |

Rates are estimates based on 2025 market data from major Canadian insurers including Sun Life, Canadian LIC, and Ratehub. Actual premiums vary based on health history, smoking status, coverage amount, term length, and specific insurer.

What term life renewal actually costs – the number most people never consider

When your term ends and you renew without a new medical exam, the insurer re-rates your premium based on your age at renewal. The policy continues — but the premium resets to reflect the actuarial risk of your current age profile. Here is what a 20-year term policy looks like at renewal for someone who bought coverage at 35 and renews at 55:

20-year term renewal comparison – $500,000 coverage

Purchased at age 35 · renewed at 55 · non-smoker

Profile

Original premium at age 35

Renewal Premium at age 55

Change

| Female non-smoker | ~$30/month | ~$250–$340/month | 8–11× increase |

| Male non-smoker | ~$40/month | ~$340–$450/month | 8–11× increase |

Renewal is designed as a short-term bridge, typically one to three years while you reassess your needs, not as a long-term coverage strategy. If you anticipate needing coverage beyond your original term, the conversion privilege is almost always a better path than renewal. If your health has changed in ways that would affect underwriting, conversion may be the only viable path.

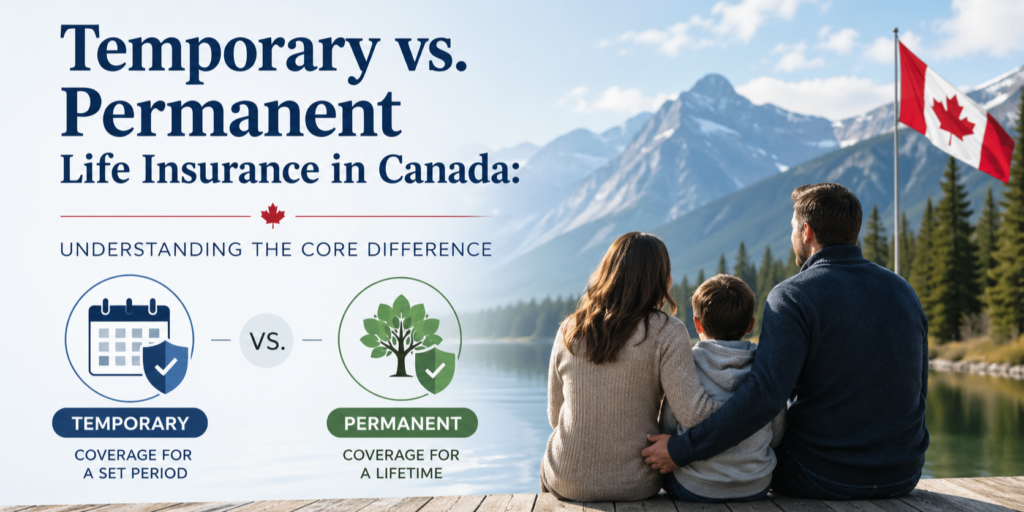

Term Life vs. Permanent Insurance: The Honest Side-by-Side

So, if my coverage will end at some point, and renewal will be so expensive, why not just buy a permanent policy? This question comes up constantly, so let us address it directly. Permanent insurance is not a single product. It is a family of four distinct products (T-100, whole life, participating whole life, and universal life), each suited to different situations. This comparison covers the category as a whole. The detailed product-by-product breakdown is in this article here.

Term Life

Permanent Insurance

| Coverage period | Fixed term (10, 20, 30 years) | Lifetime – never expires |

| Monthly cost (30-yr-old, $500K coverage) | ~$20–$30/month | ~$120–$400+/month depending on product type |

| Cash value component | No | Varies – T-100 has none; whole life and universal life build cash value over time |

| Premiums | Fixed for the term | Fixed for life, fixed for a fix term, fixed up to a certain age or variable depending on the product. |

| Best for | Temporary obligations: mortgage, young children, active debts, income replacement | Permanent obligations: estate tax liability, business succession, lifelong dependents, wealth transfer |

| Flexibility | Can convert to permanent; can layer multiple policies | Varies by product type – T-100 is simple; universal life is highly configurable |

The four permanent products explained: T-100, whole life, participating whole life, and universal life each serve a different purpose at a different cost. The full comparison is in Term vs. Whole Life Insurance: The Honest Breakdown

The math case for term: The $120–$370/month you save by choosing term over permanent coverage can be invested separately. For most Canadians, this produces better long-term outcomes than the cash value component inside a permanent policy. Most independent financial planners refer to this as “buy term and invest the difference” it is the starting framework for anyone comparing the two options for the first time. Be sure to always consider what you are protecting when making the term vs permanent life insurance decision. A permanent policy may be better suited for some of your needs.

8%

The average premium increase for every year you delay purchasing term life insurance in Canada – Ratehub.ca · 2025

Three things this rate table makes clear: women pay less (10–20% lower due to longer life expectancy); waiting is expensive (rates climb by ~8% per year); and smoking changes everything – a smoker in their 30s pays two to three times the non-smoker rate. Quit for 12 months and you may qualify for non-smoker rates from your provider.

Choosing Your Term Length

Your term should last long enough to cover the period during which your family would be financially devastated by your death. As your debts shrink, your savings grow, and your children become self-sufficient, your need for large coverage naturally decreases. Here’s a practical guide by situation:

10 yr

20 yr

25 yr

30 yr

Multiple policies vs. policy layering

Some Canadian families buy two or more separate term policies to protect different things at the same time. For example, one policy covering the mortgage and another covering income replacement. That is a valid approach, but there is another option.

Policy layering is a product structure offered by select Canadian insurers, including Cooperators. It involves a single policy (typically a permanent policy) as the foundation, with one or more term riders attached on top. Each term rider covers a specific temporary need for a defined period: a 10-year rider might cover a business loan while a 20-year rider covers income replacement during the years your children are dependent. As each temporary need resolves, the corresponding term rider lapses. The permanent base policy remains in force for as long as it is needed, covering obligations that have no expiry date. If you choose to use a term policy as the base policy, the add-on policies cannot be longer than the term of the primary policy.

The practical advantage is that your coverage shrinks in line with your actual needs over time, without requiring new underwriting or new contracts at each stage. Everything is built into a single policy structure from the start.

This approach is particularly relevant for Canadians who have both temporary and permanent needs. The family with a mortgage and young children today, but also a rental property or incorporated business that will create an estate tax obligation regardless of when they die.

Layering is worth discussing with an independent advisor if your situation involves both types of need. It is not the right structure for everyone, but for the right situation it can be meaningfully more efficient than managing several standalone policies.

5 Mistakes to Avoid When Buying Term Life Insurance in Canada

Major Term Life Insurance Providers in Canada

Canada has a well-regulated, competitive life insurance market. The premium you pay matters less than the coverage amount, the policy terms, and the insurer’s claims-paying reputation. Here are the main players:

Traditional

Traditional

Traditional

Traditional

Digital

Broker

Our recommendation: Use a comparison platform like Ratehub or PolicyMe to understand the range of rates, then work with an independent broker to finalize your purchase especially if your health history is anything other than straightforward. A broker can advocate for better rates across multiple insurers. The CLHIA and FCAC also publish excellent unbiased consumer guides.